Last week I went to the dark side. I shorted uncovered SVXY calls expiring in September.

Positions

At the time the trade was executed, 30-day synthetic was trading below 11.80.

That is an exceptionally low level, but I have been around for a long time to know that low can always become lower. However, I could not resist and pulled the trigger because the current shape of the VIX futures curve provides practically no upside for long SVXY/XIV positions.

Let’s consider the most bullish path for short vol strategies where indices continue higher and corrections are limited to less than 1%. In such a scenario VIX index will levitate around 10 whereas VIX futures curve will basically remain flat for the first three weeks of M1 contract with 30-day synthetic hugging 12. Closer to the expiration of M1 contract, M2 will move towards 12 or slightly below whereas M1 will dive down towards 10. All in all, such action would result in a slow upward move for SVXY/XIV to the tune of 2-3% from levels that were present when 30-day synthetic was at 11.80, i.e. at the time of my trade.

Rinse and repeat this same calculation for August and September and the ultimate most bullish result that I was seeing for SVXY was a maximum 10% (unsustainable) move higher from $168 through mid-September. Even if the move becomes exaggerated to the upside, the structure of the VIX curve would make SVXY/XIV vulnerable to strong pullbacks such as the market witnessed on Thursday last week.

Therefore, in my view even if I’m assigned short SVXY at $190, which given the option premium received pits my breakeven at $196.50, I believe there would be many opportunities to exit such a short position below $190 on any of market’s minimal pullbacks.

The reason I didn’t go too far out into the future, is because of my fear that VIX futures curve may reset higher should a market pullback occur in the nearest-term and after such a reset occurs the potential for SVXY/XIV to fly becomes much more pronounced should overall markets blast towards new 52-week highs after a pullback. It is much safer, in my view, to short 3-6 month expirations rather than go longer-term given the potential for short vol strategies to run higher in a low volatility environment after a VIX futures curve resets higher.

The market microstructure continues to be rather contradictory. In every update I typically make a call with regards to my personal view as to the near-term direction of the market and whether there are substantial odds of a pullback/correction. This week I am unable to make that call. I am not sure that sector rotation that we have been witnessing for the last couple of weeks means continuation of bullish conditions. I am cautious and will happily observe overall market action over the next month or two with a mostly neutral SVXY position.

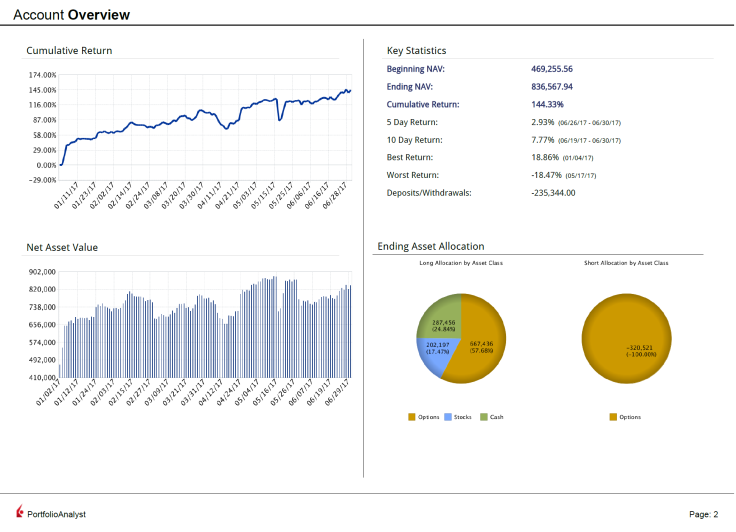

In the meantime, individual names that I have picked up during the past several weeks continue to perform in a more or less positive fashion. My trading account registered another weekly all-time high and is now up 144% YTD.

Account performance YTD

July 3, 2017 at 4:39 pm

Dear Limitless, the question about OCUL, Previously I was confused why you sold this put (above the current price). As I understood correctly You are waiting FDA approval in July and price should jump above strike.

LikeLike

July 3, 2017 at 10:04 pm

Alexey,

At the time of put sale spot was trading at $11+ and my breakeven will be $9.5 in mid-August if I’m assigned shares. I hope shares can exceed $15 before the end of 2017.

Time will tell if this trade works out. So far it’s been one of the loss-making positions.

LikeLike

July 4, 2017 at 3:03 am

Limitless,

Thank you once again for your weekly column. I have learned a lot reading each week, and appreciate your work. I had a thought regarding long dated put options on SVXY. Just as you did purchasing the long dated calls back in 2016 anticipating the run up, do you think it would be worthwhile purchasing far out of the money puts to the downside, say the January 2019 30 or 40 Put as that is where SVXY bottomed out in February and June of 2016. I know the potential return wouldn’t be unlimited as they were with your calls, but the options could definitely multiply in value should another large sell off occur before 2019. Thoughts?

LikeLike

July 4, 2017 at 7:25 am

Jason,

long-term trend of SVXY/XIV is always up due to the structure of VIX futures curve. The only way to make money on the downside is to have excellent timing. If you can get timing right then the correct trade would be buying puts for the duration of the expected correction/bear market.

LikeLike

July 4, 2017 at 1:06 pm

Hi limitless.

May i ask you how you calculate max 3 percent monthly move for svxy up if vix stays around 10? Thx in advance

LikeLike

July 4, 2017 at 5:01 pm

Dusan,

M1 would remain in mid to high 11s and M2 would remain in low 12s until one week prior to M1’s expiry. M1 and M2 weights would then be such that M1’s move from mid 11s down to low 10s would have a minimal impact on SVXY.

LikeLike

July 13, 2017 at 5:52 pm

Limitless,

Quick question: do you happen to know how the M1/M2 weightings work when the M1 contract does not start the rolling period with exactly 30 days to settlement?

For example, what if the M1 contract starts with 34 days? Or 28-29 days?

How do the M1/M2 weightings work to achieve a 30-day synthetic?

Any insights would be appreciated.

Thanks,

Chris

LikeLike

July 14, 2017 at 7:18 pm

projectoption,

my assumption is they are divided by 25 instead of 20. There are typically 25 trading days in a 5-week period (if no market holidays occur). So on Day 2 of a 35-day front month contract M1 would have a 96% weight and M2 4% weight.

But please don’t quote me on this calculation, it’s my basic assumption.

LikeLike